Creating The Path To Higher Valuation with CEO/Partner Sean Hutchinson

Many business owners flinch when hearing the word “transition.” The reason is how, for so long, it has been associated with the death of the business. CEO and Partner of SVA Value Accelerators Sean Hutchinson says otherwise. In fact, he believes that it is the path to higher valuation, making the business more valuable. With his expertise on value acceleration and transition readiness for business owners around the country, he shares the reasons why equipping yourself with the succession tools are very important. Sean talks about the three buckets or classifications of business owners that represent different points along the journey to transition readiness: explorers, pivoters, and triggerers. Learn which among these you belong to as Sean gives the three ways that you can increase the value of your business.

—

Creating The Path To Higher Valuation with CEO/Partner Sean Hutchinson

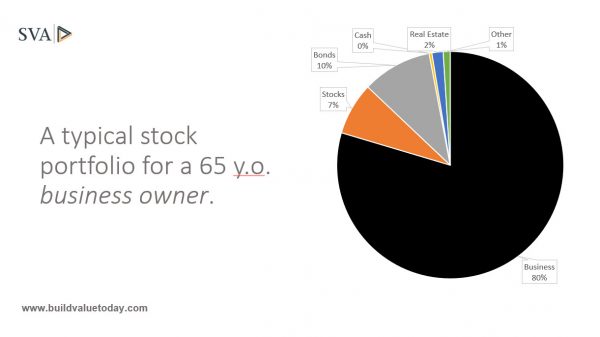

75% to 95% of the business owners’ net worth is tied up in their business, but only 10% have a plan for monetizing that net worth and only 20% will. On the show, we have Sean Hutchinson. He’s the CEO and Partner of SVA Value Accelerators. Sean, welcome to the podcast.

Thank you, Bob.

Tell us a little bit about your business and who you serve.

Our business is about value acceleration and transition readiness for business owners around the country. We only work with private businesses. We don’t focus on the publicly traded market and we work mostly with Baby Boomers, with some exceptions, that are middle-aged folks moving into the later stage of their business career. One reason why we work with Baby Boomers so often is there are so many of them. It’s a demographic that’s unprecedented in the United States. 50% of the Baby Boomers are saying that they’re going to transition their ownership in their business over the next five years. The other 50% say within ten. It’s hard to match that up with market cycles and other things. We focus on getting them ready so that they can take advantage of the window of opportunity when it’s open. The businesses tend to be in six different industries for us because we have specialty practices but they’re revenue-wise maybe $15 million to $250 million.

However, that ideal customer question had us perplexed because when people would ask, “What’s your ideal customer?” we’d start answering it in the way that almost everybody else answers it. It was “In this industry with minimum of $15 million in revenue. Business is healthy, not distressed, and so on” One day in a strategic planning meeting when we had a new advisor come on board, he asked the same question. We started answering in the same way and then somehow the conversation just stopped and we all looked at one another and said, “If the client is the owner, why are we describing our client with data about the business? Why is that the profile?” It seemed like the wrong answer and so we created what we call Three Buckets, three classifications, of owners that we think represent different points along the journey to transition readiness.

Bucket number one is the explorers. Explorers are owners who are trying to get insights and information before they decide to engage in advisory programs. They’re trying to get some clarity before they decide to spend the money, spend the time, devote the resources, to doing value acceleration and transition readiness.

The second group is the pivoters. These are the folks who have probably been sitting on their hands for a while. Procrastination is something that we all have to overcome. Whether it’s because of a life event or something else, they wake up and say, “I’ve got to do something about this.” It could be because of a business event. Things aren’t going too well in the business or something. They lose their top customer or whatever it might be that wakes them up. They pivot from inaction to action and they start moving on value acceleration and transition readiness.

The third group are the triggerers and believe it or not, we get calls from owners who wake up one day and say, “That’s it, I’m done. I’m ready to transition.” We have products and services in each one of those categories, along that spectrum. Our view has always been that we’re not trying to lasso an owner and pull them over into our world. We’re trying to go to them where they are and that’s why we had to understand the perspective of the owner about this process. Having those three buckets has helped us and it also helps us when we talk to owners. We lay it out and say, “Where would you put yourself?” Believe it or not, almost every owner that we talked to can pick one of those three things right off the bat, which tells us how to have the conversation. We don’t wander around in the wilderness talking about stuff that doesn’t matter to them.

For our audience and they go, “Transition what?” What is transition ownership?

That’s an important point and I’m glad you brought it up. For a long time, the word was, “Exit.” Exit runs into a brick wall pretty quickly because it’s got associations around it that most people don’t like to talk about.

Transition-ready businesses are more valuable.

The D word or the death word.

It connotes an end to something, which is not exactly the case. When we talk about transition, we’re talking about ownership transition but we’re also talking about the transition of the owner into the next act of their life. It truly is a transition, it’s a continuum. I respect and love owners. I’m in a third-generation family business back in Oklahoma City where I grew up. I know the stories of ownership. The things that happened along the way, the challenges that you face, the glories that you have, the victories that you can point to. This is one of the most important things that is ever going to happen in the life of a business owner, this kind of transition. Done well, there are all kinds of reasons to love it. It takes planning and it takes execution. It also takes some honesty from the owner about what they want to do next with their life.

What is their life-after-business plan? There needs to be one and it needs to be funded in one way or another. It’s like retirement, but for owners it’s a big shift in identity. I think about an entrepreneur. They’ve been doing it maybe for 35 or 40 years. They own the business. They’ve built the business. When they think about, “Who am I going to be when I am not an owner anymore?” That existential question is sometimes paralyzing and sometimes motivating. It’s a hard thing to talk about. If you place the exit as a point in time, you have to think about it differently. It’s a transition from one phase to the next phase. It’s a point in time on the journey.

When you have a business owner call you, what’s the typical range of initial questions that you get asked?

There is no typical range of questions. Every situation is different, which is another demonstration of why that first discussion is so critical. When it’s initiated by an owner, they’re expecting us to come to the table with a packaged solution in a way. When we first meet with an owner, something that often comes first in the conversation is, “What do you guys do?” We say “It doesn’t matter what we do. What matters in this conversation is your story. It’s not our story, it’s your story. That’s the one that we need to be talking about. If you don’t mind, that’s what we’d like to talk about in this meeting .” Stories connect people. If you think about your friendships, for instance, the conversations that you have with your best friends are stories. That’s how we relate to one another. That’s the only way that we can do it emotionally and with authenticity, having deep thoughtful conversations with one another.

We’re challenged in that first conversation with the owner to connect as humans, not advisers, to show that we’re interested in the story. Once we hear it, once we can get deeper into it, then we can start talking about what some steps are to get them to their objectives, whatever those might be. A lot of owners in this particular area of transition or value acceleration, it’s a black box for them in the beginning, it’s mysterious. They probably haven’t been through this process before. They don’t know where to start. They don’t know who to work with. There are all kinds of mechanical questions I suppose. The through line in all of those is, “I don’t know what to do next.” Our response is, “Let’s look at the situation, let’s have a discussion about it and then let’s decide to do one thing. Just to get started, let’s decide to do one thing. There is going to be a lot more that needs to happen in the future to get you to these objectives. We’re going to start with one, whatever might be the appropriate next action.”

Both of us are exit planning guys. You were one of the instructors at Exit Planning Institute’s most recent Certified Exit Planning Advisor course in La Jolla. My broad impression was that business owners don’t know what they don’t know. My sense is they’re so busy operating their company and they’re going to want to sell it someday. They said, “I know what it’s worth,” and then they go, “I’m ready to sell next Tuesday.” There’s an enormous disconnect between what they’ve been doing and what they understand it’s going to take to get a reasonable price for their business. You have more to say about that than I do.

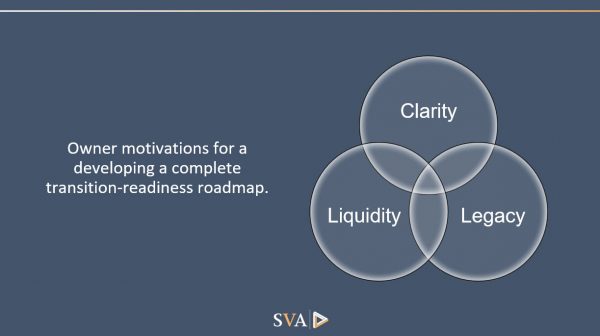

Transition Readiness: Owner motivations for a developing a complete transition-readiness roadmap

Transition Readiness: Owner motivations for a developing a complete transition-readiness roadmap

We don’t come at it from a position of, “This is a complex process. Let us fill you in on what’s going to happen next.” Our position is business owners are a whole lot smarter about their business than we’ll ever be. Our job is to enable them through this process, to facilitate the discussions that are going to be important, to help them learn how to talk about it, to understand the vocabulary, to communicate effectively internally and externally and to be honest with themselves about what they want. It’s very fuzzy when the conversation starts, for everybody. They don’t know what they don’t know. We don’t know what we don’t know. Everybody is trying to get to the same place which is clarity. We always talk in our business about an owner’s needs in this process.

The first one is clarity. That’s what we’re going for in the first stages. What are we dealing with? Let’s do some discovery. What’s the baseline here? We can look at it from our perspective. The owner has theirs, other people in the process have theirs. If we synthesize all of those viewpoints, all of those perspectives and data points, to bring together a story in a way that has not been told before, then the owner begins to look at the situation differently. The various professionals and people in their company, outside their company, family members, whatever it may be, are able to then able to paint a full picture of what the current state might be. That’s current state. The future state is up to the owner to decide. It’s our job to create a path between the two that all the stakeholders can walk together. It’s not out of reach, it’s clear, so we have clarity.

The second piece is liquidity. For most owners, that’s part of the objective. But I would say it’s not always part of the objective. If you think about a family business for instance, you’ve got multiple generations either working in the business or not working in the business. They might be children, they might be 1,400 cousins, whatever it is. Sometimes the transfer doesn’t have anything to do with money. In fact, some owners will tell you they don’t need to get any money out of it at all. They want to make sure that it transfers smoothly to the next generation and it doesn’t create undue risk for their kids or grandkids. Peaceful orderly transition to keep it in the family. For other owners, it’s all about transferring the business to an outside party and monetizing the net worth, which is usually 75% to 95% for all owners.

I’ve had a few cases where I had owners with a significant amount of wealth outside of their business but they had underestimated the value of their business, believe it or not. It’s rare. They might have $50 million in wealth outside the business with the assumption that they’ve got a $50 million business. They’re 50/50 and they’re feeling pretty good, but then they find out their business is worth $150 million and they haven’t done any planning on it. The risk allocation is not looking so good but they’re excited to find out that they’ve got more in the business than they thought. It’s the right kind of problem. The question is what are we going to do to grab that $150 million if that is important to you? Part of this discussion is always about what matters to you about money. That’s one of the core questions that has to be answered. It’s a snowflake effect. We see similarities, but every situation is so different. If you try to bake them all down into their similarities, you miss the enriched stuff around the edges, which is what counts the most. One of the things that we have to do in our practice is to learn how to synthesize huge amounts of quantitative and qualitative information.

Stories connect people. That’s how we relate to one another.

Human, financial, operational, strategic, all these things have to be combined into a story, which is going to be ongoing. You make a good point about whether the owner is working with us and asking us to help with preparation, maybe execution of some ownership transition or not. Remember we focus on transition-readiness. We don’t care in our work whether the owner is going to exit in the next year or twenty years. Our premise is that transition-ready businesses are more valuable, by virtue of the fact that they’re transition-ready. Our work in transition readiness is to get risk out of the business and to create value opportunities. The owner still has a business to run. They are still “head down.” We’re asking them to go “head up” as much as they can. In fact, there are other people in the company that we want to be “head up” and take that future state perspective. You can’t do this work if you can’t get that, at least grab some of that attention. We respect the fact that we can’t ask the owner to walk away from daily operations and work solely on transition-readiness, that would be presumptuous of us. We want to respect the fact that the owner is doing exactly what they want to do and love, which is to run a business and build a business. In most cases, they love it. In some cases, they don’t.

I’m a business owner, you’re a business owner. I’ve had a number of businesses here. I’m a fan of business owners. They have courage. I love their perspective. Their story is awesome. Part of the reason for the podcast is to record the story. The difference and a key discriminator is the business owner that maybe the one business that they’ve run and want a transition. How many businesses do you think you’ve seen the internal workings on during your career?

Probably 400 to 500. It’s a pretty big number.

For you, the perspective is when’s the last time you did something great the first time you ever did it? For the business owner, there’s that urge to say, “I’ve got my brother-in-law and my other adviser too and I can do this by myself.” Can you touch on that a little bit?

Transition Readiness: SVA Universe

Transition Readiness: SVA Universe

It happens a lot. Being an entrepreneur, there’s a certain amount of self-confidence that goes with it. That’s one of the things that drives success and we want to make sure that we build on that because you need a confident client. You need someone who’s willing to do the work and not be overwhelmed by it. That said, it can breed risk. That same self-confidence can be something of a liability. I have seen it many times. I was talking to somebody, as matter of fact, about it. He’s a successful entrepreneur. He had built a business from scratch that ended up being sold to a strategic buyer in the same industry. It was never fully disclosed, but the folks that are in that community think it was probably about a $50 million sale. He did it himself. He refused to hire an adviser. He had some lawyering around him, some accounting around him. He saved probably a couple of million, not having an investment banker in the deal, not using advisers as fully as he probably could. What do you leave on the table? How much tax did he pay that he didn’t have to pay? Were the terms and the structure of the deal built in his favor or in the buyer’s favor?

I can tell you it was built in the buyer’s favor without good advisers at the table. Whatever he left there, he left something. He certainly paid more tax than he should have and he didn’t know how to structure the deal because he’d never done it before. Entrepreneurs are self-disciplined in most cases, self-confident in most cases, maybe overconfident. Our position as advisers is always that we’re never going to ask a client to do anything that doesn’t produce both an immediate and a long-term return on investment. In our view, it’s all about creating value. We always tell our clients, “We’re never going to ask you to do anything that doesn’t add value to your business.” There is lots of stuff we can fix. There are lots of little rocks that we could pound into gravel but they don’t add value to your business. They don’t increase the transferability. They don’t increase the attractiveness to the outside market. They don’t reduce risk. They’re just things that we’re fixing in order to fix them. Let’s pick the things that matters. Let’s pick the big rocks and let’s move those rather than spending resources solving problems that don’t move the needle for you.

There are a couple of terms in there that you’ve said a couple of times. One is attractiveness, readiness and de-risking. Do you want to touch on those a little bit?

There are three ways to increase the value of a business. The one that most people focus on is increasing earnings and that’s a good one to focus on. We want to see growth in revenue. We want to see cost controls. We want to see margin in the deal and we want to see an encouraging pattern. I would always prefer to see something solid, something pretty stable rather than spikes to high profit and then falling off to a much lower level. Volatility is one of the value killers that we always look for and that’s that de-risking that we’re talking about. We’re looking at the value killers in a business and going after those first. When we work with a client, we’ll say, “Let’s look at the risks first and mitigate those to the extent that we can’t, whatever they might be.” Then we’re going to focus on driving the top line and the bottom line. You can drive top line and bottom line all day long but you may be doing it in a way that introduces risk into your business.

Let me tell you why. Let’s say that you’ve got a sales team and you send them out and they’re looking for whales. You’re a $50 million revenue business and they go find a whale that’s worth $25 million. They make the sale. To get the sale, they’ve got a discount because they don’t have as much pricing power with the whale as you do with a diverse portfolio of customers. Your sales team is excited because they accomplished what you told them to accomplish. You’re excited because your financial, at least your income statement, looks a whole lot better because you increased the size of your company by 50%, but you lost margin on the deal because you had to discount and now you’ve got one big customer that represents a third of your revenue. Your top line went up, your bottom line went up. Your gross profit probably got negatively impacted, which is a number that we watch like a hawk and the value of your business went down.

In extreme circumstances, you took a transferable business with real value in the marketplace to one that cannot transfer. In effect, you took the value from whatever it was to zero, by making that $25-million-sale. That’s counter-intuitive. To a certain extent, nothing in that strategy from a management point of view was wrong. From a value creation point of view, from the moment that the leadership directed the sales team to hunt whales, the risk was hiding under the bed and everything that happened after that was perfectly logical and detrimental to the value. There’s one story about risks that can be in the business and ways to think about them and de-risk a business. If we go in and we see customer concentration, the conversation is about how we got there. You didn’t just get lucky to land big customers. There is a team of people or process that’s making that happen. It’s not accidental. There’s risk in that process because the wrong things might be communicated.

Business owners don’t know what they don’t know.

The second thing is how are we going to address that risk? It’s not just that we’re going to tell the sales team, “Go out and find 100 new customers now, 100 little customers.” There are customer service implications to that because now you’ve got 100 customers, not ten. Are you built to handle that? There’s shipping and there’s packaging. Whatever business you’re in, the more customers you have, the more complex your business has become. It’s a whole other set of questions. We’re first looking at risk. That’s the second category of how to drive up the value of the business.

The third category is to increase marketability. This is about attractiveness and marketability or transferability of the value of the business. Let’s think about a piece of paper. That increased earnings part up at the top is going to be about two inches of the paper maybe. The reduce risk category is going to be the next five inches. It’s by far the biggest and every risk has an outsized impact either negatively or when removed positively on the value of the business. Risk impacts value much more than earnings will at the end of the day. That also is counter-intuitive because in the public markets it’s all about driving growth, driving earnings per share. The private market is not that at all. It’s all about company-specific risk and that’s why that category is so big. There’s a lot to work on but there’s also a lot of juice in working on it. It’s worth working on it. That third category of increasing the marketability of the business is about learning to communicate benchmark against your competition and be the best in class company, whatever that might be.

Interestingly for me, benchmarking data is readily available in most cases. You can get benchmarking data for $100 on a whole industry. One of the first questions that we ask when we’re getting involved with an owner is how do you benchmark against your competition? How do you stack up? There’s a story around that because owners can talk about their competition and they know a lot about them but that’s pretty qualitative. It’s good information. It’s what we would call enriched information because it’s coming out of the brain of the owner. When we ask them to scoreboard the benchmarks against their competition, they know a lot less. They probably can benchmark revenue. Everybody knows where their competition stands in one way or another. They might have gotten some information from public sources, the paper, whatever is readily available.

At the end of the day, when you start asking them questions about, “How does your balance sheet benchmark against the competition? Are you best in class? Are you middle, are you lower? How is your income statement and the various factors on it? How does your operational profile benchmark against your competitors?” The information gets a lot thinner. In order to understand marketability, you have to do one thing which will turn the light bulb on every time. That is to step outside your business as an owner and look at it through the eyes of an investor. The minute you do that, your perspective will change remarkably on how to create value. Some owners are pretty emotional about the way they manage their business and I don’t blame them because they have everything on the line. We talked about 75% to 95% of the net worth, they hold all the financial risk. There’s a reason to be disciplined and there’s also a reason to be emotionally and heavily engaged.

However, when you step outside and look at it dispassionately, try to strip away the emotion. Look at it and ask yourself a simple question. Would you buy your business? Would you buy it as it is today? Some owners might say, “Yes, I’m in.” Some owners, more often than not in the conversations that I’ve had say, “No way,” because it’s not generating a sufficient financial return to justify taking that amount of risk instead of putting my money somewhere else. That’s another benchmark in that financial return profile. Is the business performing in a way that would attract an investor? That’s when it gets down to marketability and attractiveness. No matter how attractive you think your business is as an owner, the only judgment that counts is somebody with a checkbook besides you.

Transition Readiness: SVA Game Plan

Transition Readiness: SVA Game Plan

You have a methodology, value acceleration. Let’s talk about that because, for the audience, we’re going to do a Deep Dive series on value acceleration, following this particular episode. Let’s get a bit of teaser for lack of a better term on what is that about.

We’re talking about the pivoting category. There are explorers, pivoters, triggerers. The pivoters are the ones that dive deep into value acceleration. The Exit Planning Institute, which we talked about, created a value acceleration methodology which generally breaks down into three parts. One is discover, second is implement, the third is decide. You’re going to keep it or you’re going to sell it. That’s many different conversations. We took that methodology, which we embrace, and we added a lot of value to it. SVA does it completely differently than anybody else that works in this profession as far as I know. I haven’t been able to find any other corollary. Value acceleration takes a while. Most people will tell you that it takes at least three to five years of intensive work to make significant gains. Value tends to increase exponentially. It’s not a linear process.

The curve is going to look like this…we’re starting value acceleration, we’re going to get a few gains early in the process and then we’re going to hit an inflection point where this curve is going to turn up. There are lots of reasons why it might take that exponential curve shape but you can track pretty accurately the data points, the factors that are beginning to add up to a company that can go exponential. We started thinking about the things that must be present in order to be successful, but in and of themselves do not guarantee success. It won’t happen without them, but it doesn’t guarantee success if they’re present. How many of those things would be necessary? How many of those skills, systems, whatever they might be, are there that can be chunked down into what we call 90-day sprints? That’s how we designed the program. That was what we call the design constraint. In our view, each one of these pieces of the value accelerator needs to have bookends on it.

It needs a start and then it needs a finish. We think that 90 days of work makes a big difference if you’re working on one thing during that period. If the team can break off enough time and break off enough attention and stay focused on that one thing, once we complete that, we can move on to the next. Our value accelerator is built so that what we do first supports what we do second, and that builds into what we do third and fourth. Let me walk through those things.

The first step is discovery. This is not due diligence. Due diligence is a list of stuff that you have to check the boxes on in order to be able to successfully do a deal. There’s a lot of reasons to do it because you can learn a lot about your company from doing due diligence. Discovery is different. Discovery is about asking the right questions, having the right conversations and accessing what we would call enriched information about the company and all of the stakeholders in that company. Whether it be the owner, their family, possibly the management team and other key employees in the company.

You have to enroll a pretty big group of people to do this. It’s not just going to be the owner doing the work. Discovery is important, it usually takes 60 to 90 days and what comes out of that is a whole set of information that we can synthesize and use throughout the value acceleration process. It also gives us that all important baseline. Where did we begin? What is the current state? Think current state, future state all the time. The bridge between the two is the value accelerator, point A to point B. Step one after discovery is decision dynamics. This for me was an epiphany. There are two people in our company that do decision dynamics. There are three parts to decision dynamics. One, figure out what matters together. Two, learn to make better decisions faster. Three, manage with grace and accountability. We believe that making better decisions faster is the basis of operational excellence.

No matter how attractive you think your business is as an owner, the only judgment that counts is somebody with a checkbook besides you.

If you think about it, you can drive systems all day long. You can have lean manufacturing in place. All those things can be present but if people can’t make good decisions faster, none of that can hold. We felt like for all of the things that we’re going to do in value acceleration, if people couldn’t make better decisions faster and figure out what matters together and then manage that with accountability, we don’t have the right framework for making any progress in the future. Step one, decision dynamics.

Step two, rapid risk reduction. Going back to the idea that we need to get as much risk out of the company as we can in order to prepare the foundation for that exponential value growth. Otherwise, you’re against the headwinds all the time. There is a framework for risk reduction that we use. What we’re trying to do is install or embed risk-based thinking in the organization. There are organizations that do risk-based thinking well but most do not.

Most are opportunity-based cultures ,understandably. However, risks can be classified, can be scored, and then you can decide which ones you want to take out of the company and which ones you are willing to bear. Those are decisions that are important because you will not be able to handle every risk that you find. Then the question is figuring out which one’s matter, making decisions well and fast, and then managing with accountability going forward. Let’s make sure the risks are out of the company and not just hiding over there in the corner ready to come back.

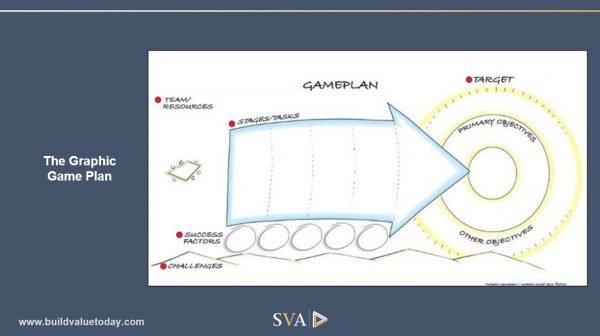

The third sprint is the company of the future. It’s all about figuring out where we want to go and how we’re going to get there.

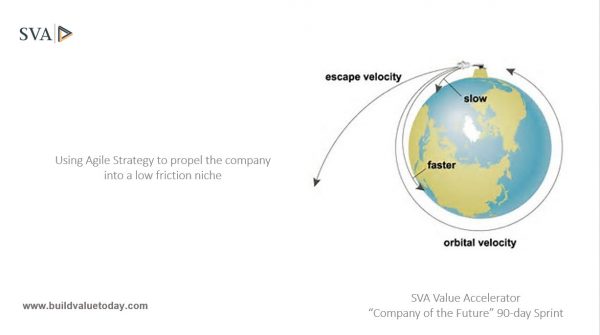

It’s a current state and future state exercise. There are tools that we use that are pretty unique. One is called the graphic game plan, the other one is called strategic doing. It’s all about agile strategy. Without decision dynamics, without risk reduction, you wouldn’t be able to do company of the future well.

After that, productivity. In a private business resources tend to be precious, capital is not always available at a relatively low cost. Here we are in the tightest talent marketplace in decades, probably going back to maybe the 1950s, constraining growth honestly. I lead the construction practice at SVA. A lot of our construction clients have great opportunities, they’ve got a huge pipeline of work, their backlog is very healthy.

What they’re not doing is growing. They’re getting pretty good margins on their projects and they’re just out of people. For organizations that don’t have productivity initiatives in place, out of 100 steps, 95 of those 100 steps may be completely unnecessary. Even when Toyota introduced Kaizen, their basis for lean, they took it from 95 unnecessary steps to 90 unnecessary steps and beat the world. If you think about your company and all of the processes, if you mapped them out and you basically started putting red X’s through the steps that don’t add value, (which is did they change form or function? Is it something that the customer will pay for?), if it doesn’t fit those criteria then it’s not needed or it’s just cost. By eliminating those steps, by doing value-add process mapping, we can identify what to take out of the company so that it can run on less, with fewer people. It’s just a more efficient productive approach.

Transition Readiness: SVA Portfolio 65-Year-Old

Transition Readiness: SVA Portfolio 65-Year-Old

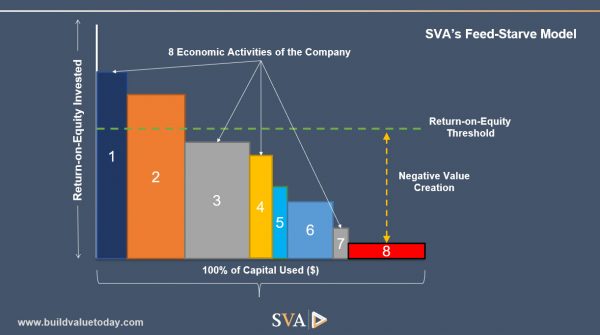

We introduced something called the Feed-Starve Analysis, which I won’t go into now because it’s pretty complex. Our productivity accelerator is the first place that it shows up in the value acceleration program and it’s going to show up again in the financial accelerator. In those first four sprints, we have now laid the foundation for operational excellence and strategy. We know where we’re going. We have a plan for how we’re going to get there. We know what our pathfinder milestones are along the way and we are becoming an agile organization that can implement strategy on a short cycle. 90 days at a time. There is no, “This is a three-year plan.” We can come up with a clear plan but we’re going to do it in 90-day cycles and then we’re going to continue doing every 90 days and see where we are. I can’t tell you how much that changes businesses. It’s remarkable. We use it in our own practice. Everything that we do in our value acceleration is something that we test in the lab of SVA and use. Practice what you preach.

Then after that is sales and marketing. We’re ready to grow. We put in place those things that are necessary for us to begin to make that exponential inflection. Many smaller companies just don’t have a sales process and don’t have a sales team. One of the big risks that sucks value out of the company is owner reliance. The owner can’t go on vacation because the company would fall apart or suffer. If you do an organizational chart, the owner somehow shows up in six of those senior position boxes. They have all the major customer relationships, they know things that the rest of the company probably wouldn’t know if something happened to the owner. Documentation may be poor, knowledge management isn’t great. Owner reliance is a lot of stuff packed into two words. When we see it, we know that there’s a whole catalog, a whole inventory, of other risks that are there.

When we go into sales and marketing acceleration, one of the things that we’re immediately going to look for is how many relationships are vested in the owner? Nobody likes to talk about it, but you have to take the perspective that bad things happen to good people. The question is do the doors shut if the owner dies or becomes substantially disabled and can no longer work? Does it keep going like nothing happened? What you want is the second. In most cases, what you’ve got is some version of the first, it’s pretty typical. Succession planning now steps into the picture. Many businesses haven’t done much and there’s a lot of work that goes into succession planning. Marketing is a mystery to most organizations. A lot of organizations think sales and marketing are the same thing. Marketability, the attractiveness of the company, has to do in part with how it manages its conversation with the marketplace, how it positions, what it says about itself, what kinds of values it has and how that’s reflected in the way it operates and produces either a service or product for its customers. It is a promise. When you are marketing, you’re making a promise. The question is can you keep it? In the sales and marketing accelerator, we can improve these things.

When you think about it, you’re wiser not taught; wiser not known.

Next, financial acceleration. The cost of capital for most private businesses is just too high. To generate a return for shareholders mathematically, you must generate a return that is higher than your cost of equity. If equity capital is 10%, you’re going to have to do better than 10% to generate a return. The company’s financial systems are not our concern unless they’re bad. Some companies struggle to put a good timely financial statement together. That can be fixed. I’m not so worried about that. What I’m worried about is the financial strategy. If we have a strategy over here that we have to execute on in order to add value to the business, everybody’s clear on that. If the financial strategy isn’t aligned with that, if we can’t get the cost of capital to a reasonable level, understand what we should be funding in the organization and what we shouldn’t, That goes back to that feed-starve thing that I talked about, what are we going to feed? What are we going to starve? The capital disperses into the organization in very inefficient ways.

Without good financial analysis and strategy, it’s hard to tell what’s working and what’s not. That goes to management reporting, benchmarking, and scoreboarding. Now we’re getting into more of the nitty-gritty.

The last thing we do which may be counter-intuitive because some people think it ought to be done first, is leadership acceleration. If we had tried to do it early in the process, to try to get leaders ready, we wouldn’t know whether we were getting the right people ready. They wouldn’t be aligned around anything. We just would have been talking leadership in a vacuum, so nobody would have had anything to hang their hat on and say, “We as a team, as leaders, are going to do this and not that.” The essence of leadership is knowing what not to do. If you’ve got people wandering around all over the place becoming better leaders, but they’re not aligned around something compelling, you have a problem.

Some value acceleration methods emphasize 90-day cycles where the owner will address five business things and five personal things. You’re definitely going to move the needle. In our value accelerator, it’s much different in terms of what we’re doing with each 90-day period. The sequencing is critical in my view. At the end of our accelerator, we have a company that’s going to look a lot different and operates a lot differently than we did in the beginning, but we at the end of two years would like to exit stage left, honestly. What we want to build is a company that can exist independently of us, that’s part of our job. We want to have been working for that period on the things that matter most to building value and creating an opportunity for the owner and other people within the company. That’s the value accelerator in a nutshell.

Part of the reason we talked about value accelerator is I want to give a broad brush. We’re going to have additional drill-down episodes that are going to deep dive into each component. That will be coming after this. First order of business for the folks that are looking to reach out to you, how do they find you?

Through our website is fine. We’re active on social media. Our website is www.BuildValueToday.com. All of our partners are on LinkedIn. We’re all active. SeanpHutchinson is my LinkedIn.

For you, there are a couple of ways that you engage. One is where you guys come in as a team and then you’re now developing a mastermind type approach.

We can do half-day workshops and full-day workshops for companies. In some cases, we’ve done it for franchise systems or corporations with distributor networks. That’s an introduction to some of the concepts that we talked about in the value accelerator. We also have mastermind groups which I’m excited about A lot of people are familiar with the Vistage model or I know there are a lot of other versions. What we thought would be useful for owners who want to focus on this idea of transition readiness and value acceleration is to create a twelve-month program, although it could be extended to 24 depends on how frequently the group wants to meet. We designed it as a twelve-month program. It’s pure owner work. If an owner is looking to be in a supportive peer driven environment with other owners, not competitors, and go through a program of twelve months that focuses on nothing but the things that we’ve talked about, then this gives them the opportunity to do that. We’re not going to be able to go as deep as we can in the full value accelerator, but we can create a DIY environment in a sense. The goal of that twelve-month program is for people to come out of it with a clear Transition-Readiness Roadmap .

.

What strikes me about this is can you imagine if they knew this before they started their business?

Almost everybody says and there are two versions of that, “I wish I’d started working on this from the beginning with the end in mind.” Then there are owners that I talk to who have been through a transition and they’ll say, “I wish I’d known you before I did that.”

Transition Readiness: SVA Feed Starve Model

Transition Readiness: SVA Feed Starve Model

People get so wrapped around the actual exit and succession. The reality is it’s just good business. When you think about that, you’re wiser not taught, wiser not known. My eyes are clearly opened up on the whole process and hence why we’re doing the podcast and that is also why we’re doing the Deep Dive. We’ve gone a fair amount of time and I typically quiz you toward the end but I’m going to abbreviate it a little bit. Is there an influential book that you like?

Let’s Get Real or Let’s Not Play completely changed the way that I think about my relationship with business owners both in the business development process and throughout what we do. It’s a great book.

Ad on page one of the local business journals sharing your message, what would it say?

It would probably say, “Transition-ready businesses are more valuable.” It would in one way or another speak to the owner around value creation and transition readiness.

For you over the past few years, what belief or protocol have you established in your company that’s helped you the most?

We move in the direction of our conversations. One of the most important things that I’ve learned in my entire life, it comes out of appreciative inquiry which is, “The things that you talk about move you in a direction either toward what you want or away from what you want or need.” We always say we move in the direction of our conversations. We say with our clients and we say with ourselves.

Transition Readiness: SVA Escape Velocity

Transition Readiness: SVA Escape Velocity

What’s an advice to a new CEO that’s assuming the role of a CEO for the first time?

Learn how to work with a Board. One of the most important parts of your job will be governance and you’ve got to understand how boards work.

Over the past few years, what would or should you have said no to and why?

Out of the hundreds of clients that we’ve dealt with, I can think of two or three that we should have said no to, which led us to improve our intake process. It’s important to have a connection with the client. We always say “connect before content” and it’s hard to do well. We can’t help a client that can’t make a good decision and some people don’t want to act. In addition, we’ve made some bad choices about who to work with. There are many things that I should have said no to as a CEO. It’s mostly related to I could have delegated that but in one way or another, I convinced myself that I could do it better and faster which was a bad mistake.

Sean, this has been awesome. I’m looking forward to doing the Deep Dive series, which is coming up next. Thanks so much.

Thanks, Bob.

Links Mentioned:

- http://BuildValueToday.com/

- SVA Value Accelerators

- Exit Planning Institute

- Sean Patrick Hutchinson on LinkedIn

- Let’s Get Real or Let’s Not Play

About Sean Hutchinson

– 25 years of experience in operations management, sales and relationship management in multinational and Brazilian companies in the service industry.

– 25 years of experience in operations management, sales and relationship management in multinational and Brazilian companies in the service industry.

– Business expertise acquired through hands-on experience in the startup of branch offices, ranging from strategic planning, definition of policies and processes, through training, development, and team management.

– Direct management of the commercial area, defining commercial policies and sales strategies, establishing goals and managing Key Accounts teams for large local and international customers.

– Extensive experience in new business development and management, customer loyalty-building, and identification of new business opportunities.

– Strong skills in contract negotiation, relationship management, cross-selling, and continuous quality improvement.

– International experience in the United States, in the hospitality and human resources segments.

Love the show? Subscribe, rate, review, and share!

Join the Business Leaders Podcast Community today:

- businessleaderspodcast.com

- Business Leaders Facebook

- Business Leaders Twitter

- Business Leader LinkedIn

- Business Leaders YouTube

The post Creating The Path To Higher Valuation with CEO/Partner Sean Hutchinson appeared first on My podcast website.